DB's Jim Reid has released his "2018 Credit Outlook". In our first pass on this 60-pager earlier, we noted that Reid characterised 2017 as the most "boring year ever", since it will go down as one of, if not the least, volatile year for the majority of asset classes.

Heading into 2018, Reid characterises risk assets as a tightrope walker who's successfully negotiated a hire wire since the 2008 crisis. However, the confidence of our risk asset funambulist was always fortified by the knowledge that there was a huge safety net direct beneath him in the shape of the central bank put. In Reid's own words.

The best analogy for our view on 2018 is that risk assets are like a highly skilled but still relatively inexperienced tightrope walker. Our tightrope walker started his career immediately after the GFC and earned his apprenticeship in very difficult conditions with lots of crosswinds but with the knowledge that a huge safety net existed beneath him. This allowed him to walk across the narrow line with slow but ever-increasing confidence, skill and aplomb. In our analogy the safety net is the central bank put that has continued to help financial markets' confidence over the last several years in spite of very challenging conditions.

As the tightrope walker steps from December 2017 into January 2018, he's going to notice a disconcerting change in his safety net.

However in 2018 our tightrope walker will have to move onto the next phase of his career where the structural support of the safety net will likely be slowly weakened. Every time he looks down he'll figuratively see a central banker loosen or take away a supporting rope. As such his skills and confidence are likely to be tested more than in recent years.

Reid is specifically referring to the growth in the size of the big four DM central bank balance sheets, i.e. the Federal Reserve, ECB, Bank of Japan and the Bank of England. At the end of 2017, the combined size of the big four's balance sheets is estimated to reach about $14.9 trillion, an increase of about $1.8 trillion on the end of 2016. That's about to change radically, as he notes.

Assuming fairly neutral and consensus assumptions, central bank balance sheet growth will fall sharply over the next 12-24 months from the near peak levels currently seen.

The chart below shows that on a rolling twelve-month basis, growth will fall sharply, beginning in 2Q 2018. By the end of 2018, DM estimates that the rolling twelve-month growth will have declined about 75% from its 2017 level to about $450 billion. By August 2019, growth will have declined to zero according to DB's estimate.

As the report notes, this "represents a changing of the guard for ultra-easy policy". The problem for Reid's tightrope walker is that he's come so far, there's no turning back, even if he knows the risk of a catastrophe is only going to increase for the best part of the next two years. From Reid's perspective, the threshold in terms of higher risk will be crossed as we move from Q2 2018 in the second half of next year.

So barring an external shock the ECB will be relatively dormant until late in Q2 when speculation will start to mount about what comes next after the current QE extension to the end of September 2018. DB's expectation is for a quick and full taper in Q4 and the first policy rate hike in June 2019. As such, as we approach the June meeting - which will probably be the earliest that any announcement will occur - more hawkish speculation will likely start to mount about the future of the program. Indeed by the time we get to H2 2018 we'll potentially be seeing a very different global QE picture to that we've been used to in the recent past. By then the Fed will be well into its gradual, but slowly increasing run down of its balance sheet.

As the report notes, the slowdown in QE purchases in 2017 will likely coincide with significantly different conditions to the most recent example in 2014-15.

While markets went through similar balance sheet wind downs through 2014 and into 2015 - driven predominantly by the Fed and ECB - not only was the stock of global QE lower with less central banks conducting such operations, we also had a situation where the tapering was consistent with a reduction in government issuance.

Fast forward to 2018 and a reduction of purchases across the globe could be occurring at a time when there is a move to increase government spending even if this isn't yet showing up in the forecasts. The US tax plans haven't been finalized as we go to print but an unfunded tax cut is our base case which will add to the deficit and eventually to treasury issuance. In the UK the budget - seen just before we went to print - included some loosening of the fiscal purse, as the current administration deal with Brexit risks and a population tired of austerity. Even in Germany, the recent election uncertainty and eventual coalition could include some fiscal stimulus.

So we think the tide is turning away from ultra-loose monetary and relatively tight fiscal even if the official fiscal forecasts from most commentators are yet to include much in the way of easing across the globe.

Reid backs up his forecasts with charts for the three key central banks, firstly the Federal Reserve and the Bank of Japan. The chart for the Fed shows that its purchases of Treasuries have never exceeded net supply. In contrast, the BoJ has exceeded net supply during the last four or so years of Abenomics, although the ratio has stabilised at around three times.

Turning to the ECB, the change in ECB purchases versus net issuance will be dramatic as 2018 unfolds.

Reid argues that.

Interestingly, if we look at the Fed, BoJ and ECB Government bond purchases versus net supply of domestic Government bonds we can see how the ECB's removal of QE could be very different to that of the Fed relative to when it started tapering. In addition the supply/demand dynamic for European Government bonds has recently been even more extreme than in Japan…as ECB purchases have recently been seven times net issuance at their recent peak.

So in other words we've seen the huge PSPP volume far outstrip the relatively negligible net issuance in the Euro area. While the Fed program was clearly huge in absolute terms, relative to supply it was much more modest. It also declined along with Treasury issuance meaning that yields could be sheltered from the tapering impact.

In Europe we could see government bond QE go from seven times net issuance in Q3 2017 to more in line with it by the end of 2018. As the realisation mounts that ECB QE withdrawal is much more significant in relative terms to that seen in the US in 2014 then fixed income markets could become more vulnerable which may in turn create more volatility and more difficult conditions for credit spreads.

Which…unless we are missing something…sounds very bearish for European credit.

Nonetheless, when it comes to the DB team's central case for credit spreads in 2018, they are relatively benign. Indeed, DB expects a tightening in Q1 2018, followed by a modest widening from Q2 2018 to the end of the year.

As the report notes, team member "Craig" is more bearish than his colleagues and his views seems more in keeping with the general thrust of the report.

Combining the net purchases versus net issuance data for the Fed, ECB and BoJ, Reid notes.

When we combine these three central bank purchases with net issuance historically in Figure 18 we can see just how supportive the technicals have been for government bonds. This is seemingly peaking out at the end of 2017 and with our forecasts for central bank purchases and a continuation of the 2013-2017 reduction in Government bond net issuance we expect this now to reverse. For choice we think fiscal spending will start to pick up which means these net issuance estimates are probably too aggressive on the downside.

Once again, the correct conclusion would seem to be bearish, although DB seems reluctant to go there. We are even more perplexed when DB cites the risk that inflation will surprise on the upside.

Meanwhile we think the risks to inflation are on the upside…will likely mean that crosswinds pick up as we move through Q2 and into H2 – a period where US inflation might start to more consistently beat on the upside (or at least not consistently miss on the downside) and markets start to think about a June ECB meeting where the end of Euro QE is possibly announced.

Returning to his metaphor of the tightrope walker, DB notes the probability of him remaining on his wire will deteriorate as the year progresses.

If we're correct on inflation it's going to be difficult for central bankers to justify anything other than the slow and steady removal of the safety net beneath our intrepid tightrope walker. As such his task will get more difficult purely because his confidence must surely weaken with more risks associated with any fall. As such he's likely to wobble more. So expect volatility to finally start to increase after surprising many by staying as low for as long as it has done. At this stage the tightrope walker may have enough skill to safely navigate across to the next point (end 2018), however the probabilities of such a successful outcome are likely to be getting lower as the year progresses.

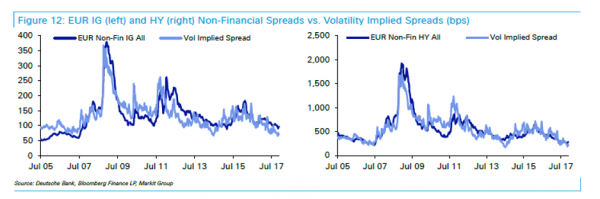

Perhaps Reid has been dissuaded from taking a more bearish stance by the ultra-low environment for volatility which he noted had made 2017 so boring. Indeed, he notes the close correlation between major asset volatility levels and credit spreads.

As we noted in our first pass on DB's "2018 Credit Outlook"

Reid joins countless other strategists opining on the lack of vol in the past year, asking "why has volatility been so low and can it continue?" His answer is that the most likely reason for volatility being so low is a combination of:

Synchronised and firm global growth;

Inflation that has consistently been in the 'Goldilocks' range and not accelerating as much as expected in 2017, and;

Global central bank liquidity which in 2017 has still been close to peak levels.

What Reid neglected to mention is that volatility has itself become a tradeable input – making it reflexive in nature - and one which has been shorted to insane levels, both implicitly and explicitly.

The rapid elimination of the central bank security net coupled with rising inflation are transforming the risk profile for Reid's tightrope walker, as he acknowledges, and one where the chances of a sustained spike in volatility must be commensurately higher. We know from his writings that Reid is a big Liverpool (soccer) fan, as are we. It's been a frustrating season so far. So often, the build-up play has been excellent while putting the ball in the back of the net has been elusive. We felt like this about DB's otherwise impressive report.