It's all about the magic.

Firstly, following up on the Liquidity Wave: Mario Draghi followed through on his primary mission and did not upset markets. Indeed Super Mario gave the $DAX virtually all of its price gains for October:

Magic.

Just so we're still clear who's running the price discovery show in global markets:

Central bank balance sheets have expanded by $4.5 Trillion since the beginning of 2016. pic.twitter.com/wh4mBVl99D

— Sven Henrich (@NorthmanTrader) October 27, 2017

Magic.

You do realize that Mario Draghi's term is ending in 2019. Which means he will have never raised rates once during his entire tenure. He came, he saw, and he was easy. And stayed easy. And then went on to cushy speaking engagements. Magic.

Next in the line of magic: Tech.

Tech flew to new highs on Friday on the heels of earnings reports and markets celebrated Jeff Bezos becoming the richest man in the world with a $90B net worth.

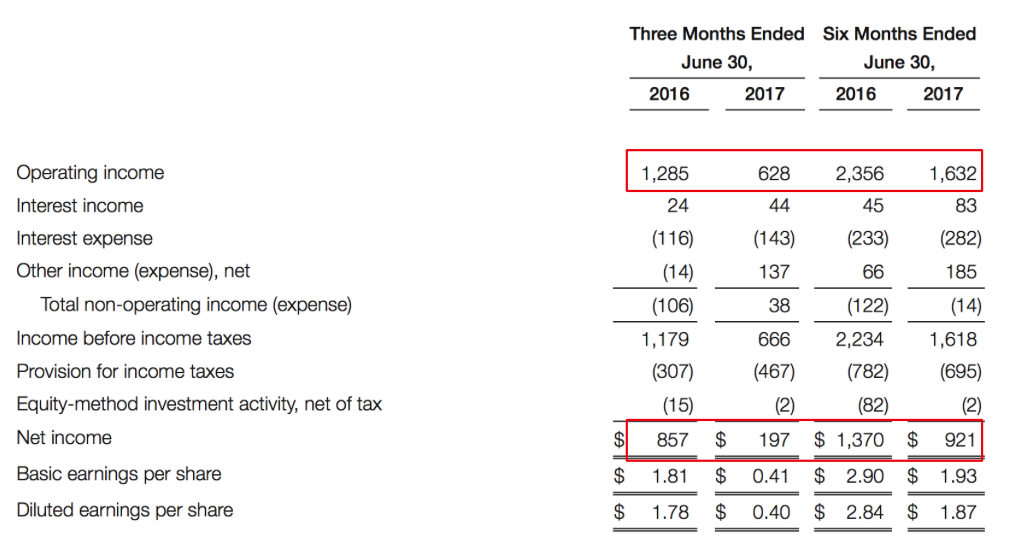

Magic. Cause it was all done with a shrinking earnings picture:

Operating income cut in half and net income 23% of what it was last year. But hey, disruption and destruction of the entire retail space as we've seen 6,700 store closings already in 2017.

So one company kills the margins for everyone else, has an operating margin of virtually zero itself, but hey, magic:

Indeed the real magic is in market cap expansion. It is true the tech monopolies are killing it in terms of growth and market share, but the market cap expansion that comes with it is awe inspiring.

Someone ran the math:

AMZN, GOOG, MSFT, INTC

Value today: $2096b

Value 1y ago: $1592b

Increase in value: $504b or 31.7%

Increase in earnings: $2.2b https://t.co/bH1J8bCKKC— Anil (@anilvohra69) October 29, 2017

AMZN now has a market cap of $528B with a PEG ratio of 4.77. But it's not about valuation and it's clearly not about earnings. It's about magic.

So tech screamed to new highs on Friday.

Watch the magic:

New Highs vs New Lows on Nasdaq:

$NDX stock above their 50MA:

I take it you noticed that sinking feeling.

But it's not only tech, it extends to the entire market:

$SPX:

$NYA:

Indeed the new highs on Friday?

Came on a negative $NYMO:

The entire new highs picture since September has come on lower and lower $NYMO readings.

Check recent cumulative advance/decline:

New highs on running cumulative negative advance/decline issues.

And all of this of course is reflective of a long standing trend in equal weight that just fell off the cliff:

But hey. Time for tax cuts, the top 1% are suffering:

Tax cuts now!https://t.co/yY6q7TD9wT

— Sven Henrich (@NorthmanTrader) October 27, 2017

Convincing voters that these folks need tax cuts so that they themselves may fare better may indeed be a true magic act.

But that's what everyone is waiting for I'm presuming. After all this would be the reason why investors are fully long positioned per the Rydex bull/bear ratio, now at 0.05:

With valuations in the 99th percentile of history:

And planning to add more and more and more:

Yes, everybody loves magic. Just remember magic levitation may simply be a cheap trick with someone pulling on a string:

SPOTTED: Magic levitation may not be so magic. pic.twitter.com/XSKzo1XjgX

— Sven Henrich (@NorthmanTrader) October 29, 2017

Next week we will get to see another magic show: The FOMC will tell us why they can't raise rates again and we will find out who Janet Yellen's replacement will be.

I'm sure it will be magical.