Given the state of affairs in his beloved European Union right now Mr. Juncker and company are doing a lot of lying.

It is rare in politics to get that kind of honesty from a politician, especially one currently in office. But, Juncker's statement shouldn't be a surprise to anyone who is even a semi-serious political observer.

It's why I find it funny that the Democrats and Antifa-Left get so bent out of shape when Donald Trump exaggerates or outright lies. To him it's a tactic. Catching Donald Trump in a falsehood is like trying to ladle water with a sieve.

So, by the Juncker Maxim, things must be getting very serious because the amount and type of lies being thrown around by people who are supposed to know better have been staggering.

To the point that Russian Foreign Minister Sergei Lavrov said, "I simply don't have any normal terms left to describe all this."

Lavrov has been the world's most effective diplomat over the past few years, effectively talking to and cutting deals with people who should hate him and Russia's policies. What it highlights is that Lavrov and his boss, Vladimir Putin, have been effective simply because they make a deal and keep to it.

They are the opposite of Mr. Juncker. When things get serious they become honest, speaking with one voice.

Part of that comes from having a single administration in power for the past 17 years. It's easy to keep to agreements when those in power don't change. The U.S.'s diplomatic history with North Korea, for example, highlights the problems of shifting domestic political winds in Washington.

But, that part stems from the way these men comport themselves on international stage.

So, watching the hyperventilations of of Theresa "Gypsum Lady" May and her Foreign Secretary Boris Johnson over the poisoning of Former Russian double-agent Sergei Skripal and his daughter Yulia means there is a lot more going on here than anyone cares to admit.

The quick reversals from European leaders as well as Donald Trump from their initial skepticism of May and Johnson's bloviating tells me that not only are they lying but they are being forced to lie by some vaguely unseen hand.

Just Blame Putin-stan!

It's not just that the Neocons are losing, like I talked about in my last article. It is that stench of desperation that's everywhere right now.

The level of histrionics, lying and insanity over Former Assistant FBI Director Andrew McCabe's firing is telling. From McCabe himself, to his disgraced former boss, James Comey, the level of mendacity, chutzpah and, frankly, evil on display is impressive.

I guess the situation's been serious for a long time for the lies to come this easily to their tongues.

This week we had the staged walk-outs by high school students over the Parkland, Fl shooting calling for gun control. How desperate are those clinging to power behind the scenes that they've turned to weaponizing mal-educated children to do their bidding?

His Ideas Resonated Better in the Original German

The French Foreign Ministry instructing its diplomats to not travel to Syria is also telling. It's all about lying to support the narrative that Assad and Putin are the bad guys.

The Reuters article I just linked to spends more column inches perpetuating the lie that there are no humanitarian corridors in Eastern Ghouta, Syria, even though there are plenty images, video and reports of thousands of civilians having been liberated from ISIS/Al-Qaeda-linked jihadists.

But it mentions reports of chlorine gas attacks, again neglecting to say anything about the Syrian Army liberating a major chemical weapons facility in their advances against US-backed proxies.

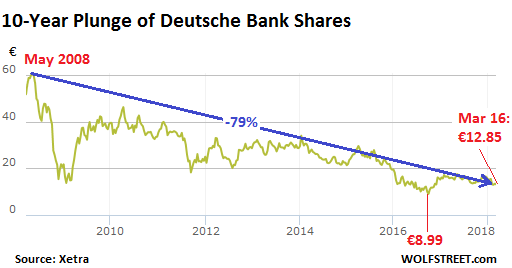

How bad is the situation behind the scenes in the financial markets that Goldman-Sachs CEO Lloyd "Doin' God's Work" Blankfein suddenly decides it's time to step down? Derivative book that bad, Lloyd?

Or did you bet that Gary Cohn would get Trump to heel to allow Goldman to finish destroying Europe?

Long-established diplomatic norms and rules of conduct are simply thrown out the window because they need to be to induce hysteria to take people to war, otherwise, a war-weary, anxiety-ridden population will turn on their own governments.

So, Theresa May tells Russia to prove to her they're innocent to distract from her betrayals on Brexit.

This is a joke, Right?

Boris Johnson threatens Putin directly and the moron in charge of Britain's defense department screeches for the Russians to 'shut up and go away.' Presumably he said it from his safe space rubbing his safety pin like Captain Queeg.

Meanwhile Mr. Juncker continues to lie about everything as it pertains to Brexit negotiations because the EU's financial situation must be that serious. If it weren't they wouldn't be trying to shake the U.K. down for tens of billions of euros.

Why So Serious?!

Look around you, step back from the craziness and see the bigger picture. When you do you just see a bunch of incompetent, venal people covering their asses. While a lot of what I write here could be considered 'conspiratorial' I would disagree.

In fact, I rarely, if ever, chalk up to conspiracy that which incompetence explains far better. As a root cause analyst, I prefer Occam's Razor to Alex Jones.

Yes, there are groups of people with power conspiring to achieve personal and societal goals which are anathema to life and decency.

But, that doesn't mean that because they have power they are competent at wielding it. In fact, power makes you lazy. Winning makes you complacent and, eventually, stupid.

Does anyone with any shred of self-respect believe that thirteen Russian trolls armed with Tweetium could derail Hillary Clinton's presidential campaign? Really?

When the more obvious answer is that Hillary and her backers thought they had perfected the art of rigging an election and never conceived of losing. It never crossed their minds until a few days before the election and internal polling forced Obama to campaign in Michigan on her behalf.

And he only did that to help himself, since he was in up to his neck in all of her dirty laundry.

The Theory of the All-Powerful Putin is a childish and nonsensical as the Alt-Right's blaming Jews for everything.

The Gypsum Lady is trying to save her government by invoking it now. So is Nikki Haley at the U.N., Mika Brzezinski at MSNBC, George Soros and David Brock, the leadership at CNN, Google, Facebook and Twitter. The bigger the lies get, the more desperate you know they are.

All of the Obama administration traitors — Samantha Power, James Brennan, Susan Rice, Robert Mueller, Comey, McCabe, Eric Holder, etc. — lie every time they open their mouths. It their narrative fails it means the end of not only their careers, but the plans of the incompetent globalist oligarchs who fund and power them.

And those are the stakes in play here.

Ye Gods, and I haven't even brought up the Saudi Arabians, yet. Or the attempted military coup against the U.S. pet in Ukraine, Petro Poroshenko, from within his own government, no less.

Talk about gross incompetence!

Cooler Heads or Heads in a Cooler?

While I'm not sanguine about how all of this plays out, I refuse to give into hysteria and add to the cacophony. It serves no purpose.

The markets still believe, as they always do, that 'cooler heads will prevail.' But, markets aren't allowed to believe anything else. The central banks ensure that. The sheer size of the money at stake makes it nearly impossible to move much of it without inducing even more panic.

So, the default position of most money managers is sit tight and hope.

But, hope is not a plan or a path to the stars. It is, as I've said before, the worst thing in the world — that which you have when you have nothing else. But, changes are coming, war or the collapse of the post-WWII institutional order or both.

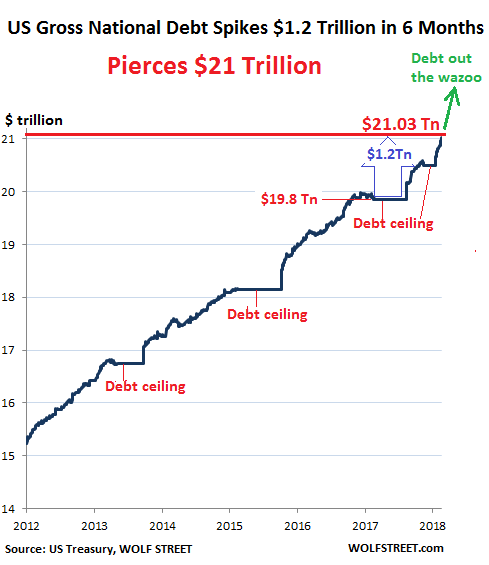

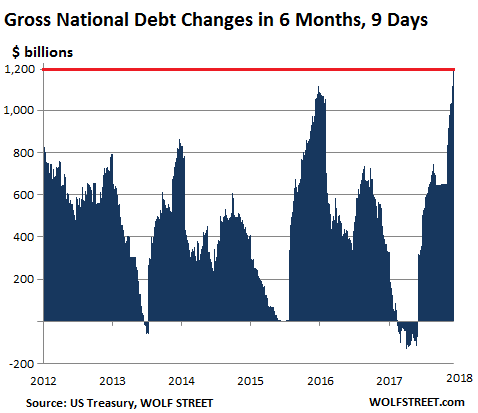

As I've pointed out, banks are getting nervous, emerging market central banks are positioned for radical currency defense. Rates are rising and dollar liquidity is falling. Bitcoin and gold are screaming this. If there was ever a time to get to cash it's now.

The acceleration of events since Putin's speech on March 1st is itself accelerating. Windows are closing fast. It's time to get serious.