Sometimes you don't know how deep the hole is until you try to fill it. In 2009, staring down what looked to anyone with a calculator like the biggest financial crisis since 1929, the federal government poured $830 billion into the economy — a spending stimulus bigger, by some measures, than the entire New Deal — and the country barely noticed.

It registered the crisis, though. The generation that came of age in the Great Depression was indelibly shaped by that experience of deprivation, even though what followed was what Henry Luce famously called, in 1941, "the American Century." He meant the 20th, and, to judge from our present politics, at least — "Make America Great Again" on one side of the aisle; on the other, the suspicion that the president is a political suicide bomber, destroying the pillars of government — he probably wouldn't have made the same declaration about the 21st. A decade now after the beginning of what has come to be called the Great Recession, and almost as long since economic growth began to tick upward and unemployment downward, the cultural and psychological imprint left by the financial crisis looks as profound as the ones left by the calamity that struck our grandparents. All the more when you look beyond the narrow economic data: at a new radical politics on both left and right; at a strident, ideological pop culture obsessed with various apocalypses; at an internet powered by envy, strife, and endless entrepreneurial hustle; at opiates and suicides and low birthrates; and at the resentment, racial and gendered and otherwise, by those who felt especially left behind. Here, we cast a look back, and tried to take a seismic reading of the financial earthquake and its aftershocks, including those that still jolt us today.

AMERICA STOPPED BELIEVING IN THE AMERICAN DREAM

By Frank Rich

If you were standing in the smoldering ashes of 9/11 trying to peer into the future, you might have been overjoyed to discover this happy snapshot of 2018: There has been no subsequent major terrorist attack on America from Al Qaeda or its heirs. American troops are not committed en masse to any ground war. American workers are enjoying a blissful 4 percent unemployment rate. The investment class and humble 401(k) holders alike are beneficiaries of a rising GDP and booming stock market that, as measured by the Dow, is up some 250 percent since its September 10, 2001, close. The most admired person in America, according toGallup, is the nation's first African-American president, a man no one had heard of and a phenomenon no one could have imagined at the century's dawn. Comedy, the one art whose currency is laughter, is the culture's greatest growth industry. What's not to like?

Plenty, as it turns out. The mood in America is arguably as dark as it has ever been in the modern era. The birthrate is at a record low, and the suicide rate is at a 30-year high; mass shootings and opioid overdoses are ubiquitous. In the aftermath of 9/11, the initial shock and horror soon gave way to a semblance of national unity in support of a president whose electoral legitimacy had been bitterly contested only a year earlier. Today's America is instead marked by fear and despair more akin to what followed the crash of 1929, when unprecedented millions of Americans lost their jobs and homes after the implosion of businesses ranging in scale from big banks to family farms.

It's not hard to pinpoint the dawn of this deep gloom: It arrived in September 2008, when the collapse of Lehman Brothers kicked off the Great Recession that proved to be a more lasting existential threat to America than the terrorist attack of seven Septembers earlier. The shadow it would cast is so dark that a decade later, even our current run of ostensible prosperity and peace does not mitigate the one conviction that still unites all Americans: Everything in the country is broken. Not just Washington, which failed to prevent the financial catastrophe and has done little to protect us from the next, but also race relations, health care, education, institutional religion, law enforcement, the physical infrastructure, the news media, the bedrock virtues of civility and community. Nearly everything has turned to crap, it seems, except Peak TV (for those who can afford it).

That loose civic concept known as the American Dream — initially popularized during the Great Depression by the historian James Truslow Adams in his Epic of America — has been shattered. No longer is lip service paid to the credo, however sentimental, that a vast country, for all its racial and sectarian divides, might somewhere in its DNA have a shared core of values that could pull it out of any mess. Dead and buried as well is the companion assumption that over the long term a rising economic tide would lift all Americans in equal measure. When that tide pulled back in 2008 to reveal the ruins underneath, the country got an indelible picture of just how much inequality had been banked by the top one percent over decades, how many false promises to the other 99 percent had been broken, and how many central American institutions, whether governmental, financial, or corporate, had betrayed the trust the public had placed in them. And when we went down, we took much of the West with us. The American Kool-Aid we'd exported since the Marshall Plan, that limitless faith in progress and profits, had been exposed as a cruel illusion.

A Decade After the Crisis: The Lingering Effects

IT WAS BAD — REAL BAD

China, September 16, 2008. Photo: Brendan McDermid/REUTERS

Total U.S. household net worth dropped by $11.1 trillion in 2008.

The median income for 25-to-34-year-olds in America, $34,000, hasn't budged since 1977, adjusted for inflation.

Median household wealth collapsed.

2007: $126k

2016: $97k

The number of Americans worried about the economy multiplied nearly sixfold.

2007: 16 percent

2008: 86 percent

In 2016, the median wealth of a family headed by someone born in the 1980s was 34 percent below the level of earlier generations at the same 2007: age.

Mutual funds lost a third of their value: -38 percent.

The market value of all publicly traded companies was cut in half.

October 2007: $63 trillion

March 2009: $28.6 trillion

From 2005 to 2009, the median value of stocks and mutual funds owned by whites dropped by 9 percent.

The median value of holdings for African-Americans dropped by 71 percent (probably because of pressure to sell when prices were low).

Between 2007 and 2013, wages declined for the bottom 70 percent of all workers.

The retirement savings of black families fell by 35 percent from 2007 to 2010.

In a 2016 survey by the Fed, 28 percentof working-age adults said they had no retirement savings whatsoever.

The racial wealth gap, already large, ballooned.

Whites: $171k

Hispanics: $20.7k

African-Americans: $17.6k

In terms of household wealth, every group suffered — but some more than others.

Hispanics: -66 percent

Asian-Americans: -54 percent

African-Americans: -53 percent

Whites: -16 percent

Consumer credit-card debt at the end of 2017 was over $1 trillion (about 30% higher than in 2008).

Millennials have taken on at least 300 percent more student-loan debt than their parents' generation.

The unemployed took many more weeks to find work.

May 2008: 7.9

June 2010: 25.2

In a December 2017 poll by YouGov, 38 percent of those surveyed said they didn't know when they'd be debt-free. 30 percent of respondents thought they'd never be out of debt.

63 percent of Americans say they don't have enough money in savings to cover a $500 health-care expense.

In 2017, women had nearly 500,000 fewer babies than in 2007, although there were 7 percent more women of prime childbearing age.

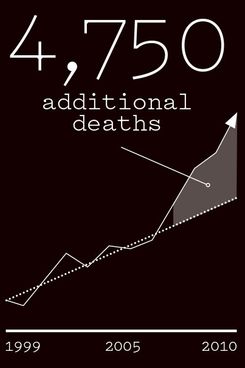

The suicide rate rose 4 percent from 1999 to 2010: 4,750 additional deaths.

24 million adult millennials, or 32 percent, still live at home.

79 million Americans live in a "shared household" with at least one extra, nonfamily resident.

More college grads moved in with their parents.

2005: 19 percent

2016: 28 percent

As of 2017, only 34.2 percent of homes have recovered their value from before the recession. (Still below 2008 value.)

From 2000 to 2015, homeownership declined in 90% of all U.S. metropolitan areas.

Reporting by Joy Crane and Matt Stieb

WTF HAPPENED?

Sheila Bair

Former head of FDIC

Once the system was stabilized in early 2009, we had an opportunity to restructure and break up Citigroup in particular, but we didn't do that. I think that was a missed opportunity. We just reinforced too-big-to-fail with all these bailouts, let's face it. Other than Lehman Brothers, nobody took their medicine. Restructuring Citigroup would have sent a powerful signal that the government had the gumption and courage to stand up to these very large institutions, and to impose losses on bond holders.

I think we've improved the system on the margin. There are higher capital requirements, there's better bank liquidity, less reliance on short-term financing, less reliance on debt among the regulated banks. Those are all positive things. But the financial system we have is still basically the financial system we had in 2008, with more capital and less reliance on short-term funding, so whether it's enough? I hope it is.

I wish we had more Republicans who would stand up to these cronies who want the government bailouts. I think a lot of people still want that on Wall Street — it's secretly what they want. They think it's the government's obligation to keep them afloat. I'm a capitalist, and I'd rather have the state own them than have that system.

It's very frustrating. It's just stupid economics. Set the morality aside; it's just dumb economics to have a system like this where you're propping up inefficient, bloated institutions. So there are good economic reasons to not have the system we had in 2008, and whether we've gotten rid of it or not I don't know. I think we won't know until a big bank gets in trouble again. Then we'll see what happens. I don't even want to think about what the political fallout would be.

Corey Robin

Political theorist

The first and most obvious fallout is that in the '90s and the '80s — when pensions were being switched over to 401(k)s — there was a strong sense that the stock market really was this kind of profound divination and assurance of all well-being. You've got a whole generation of people, my generation and even a little bit older, whose entire futures are caught up in — if they're lucky, by the way — 401(k)s and the state of the stock market. It really knocked the wind out of the fundamental belief that the market would take care of things.

A couple weeks ago, a friend on Facebook who's in advertising — and who's not a political person at all — posted something: Hey, guys, what are we all thinking about retirement? And it was just shocking, the unanimity among everybody, that retirement was not something that would ever happen. And these are people who are upper-middle class, professional managerial class, and not thinking of working forever because work is fun.

The triumph of the neoliberal consensus, post-1989, was to naturalize the economy. Here are these laws that are fairly apolitical, untouchable, the equivalent of the laws of nature. What the financial crisis, and then the response to the financial crisis, did was to denaturalize that again. So suddenly the economy looks political. The combination of the stimulus package and Obamacare threw open all over again the possibility of government intervention in the economy in a way that had seemed very much closed off, permanently, for a generation. But while [the stimulus package and other measures] restored some kind of basic semblance of health in the economy, all of the fundamentals about wages in particular remained pretty much the same. Our economic situation as a lived experience has not changed and is as fundamentally precarious as it was before. And that's a very explosive situation.

You know, Tocqueville has this very famous argument in his book on the French Revolution, where he says it's not steady immiseration that creates the conditions for revolution. It's actually situations that are kind of getting better but not getting better fast enough. That's when people start looking at more radical alternatives.

Robert Shiller

Economist

I was in a panel around 2005 when an economist from Freddie Mac said that they do stress tests and they're safe. I was raising the possibility that home prices might fall. He said, "We have taken simulations that go as far as a 13 percent drop in home prices, and we can survive that." I'm paraphrasing him.

So then I said, "Well, what if it falls more than 13 percent?" And he said, "They've never fallen more than that, not since the Great Depression." And so I said, "Well, what about that? It happened in the Great Depression." He sort of made me look like a fool for saying that could happen. So these things become so remote that they become storybook-land, and then we set ourselves up for another one.

People learn things — sort of — and then years go by, and there are new success stories that people hear about and they want to be part of it. And then people who warn them about getting overexposed, as more years go by, start to look like losers.

One thing that has brought back some of the old feeling is the fact that we've set new records for home prices in nominal terms and the stock market, so it provides some sense of vindication for those feelings of ten years ago. We've had three big peaks. One was in the year 2000 in the stock market, and then in 2007 in the stock market and the housing market. And then now again, both the stock market and the housing market are at record highs. So the sense of humiliation is fading, and the sense that the 2000s, before 2007, was a mistake is fading.

I don't think that we can protect people from human nature. We have a stock market, which is on its own. Way back in the 1930s, they put on margin requirements to prevent you from borrowing too much to buy stock, but that didn't stop us. And so you plug holes, and then it's like the Dutch boy and the dike. Another one springs because there's a basic human drive, a speculative drive. So to some extent we have to let people make their own mistakes. Along the way a lot of great things happen.

Matt Bruenig

Policy analyst

The main legacy of the Great Recession is going to be accelerating the concentration of wealth. I have a figure that's going to come out in our next report that says between 2007 and 2016, the average wealth of the top one percent increased by $4.9 million at the same time as the wealth of the median family declined by $42,000. The wealth is being sucked out of the middle and pushed to the top. That's what you would expect from the type of bailout that they did. They let homeowners drown and they bailed out financial institutions whose shareholders are mostly very affluent families.

Young people who came into working age, they face permanent repercussions because they can't get jobs, or if they can get jobs, the jobs are not paying that well. And of course a lot of them are putting on more and more debt if they're getting a college education.

And so you kind of get a lost generation of sorts. A mild lost generation. You know, like they weren't killed in a war. And one of the ways that you see this effect is a drop in fertility. There was a very marked decline after the recession. And that's mostly young adults who obviously are making an economic decision that they can't afford children. And you don't recover from that.

And obviously there's a racial component too that I feel has been very overlooked. I don't think people realize just how bad the Great Recession was for black and Latino families. The level of wealth decline in those groups … You could write a whole reparations article just off what happened in the past eight years. Like, you don't even need to go back to the GI Bill. You could just say, "Look at what happened where clearly racially predatory bankers load black families up with these subprime mortgages and just extract wealth out of them." That's the story that's not been fully discussed, for one reason or another.

Yves Smith

Founder, naked capitalism

Trump is crowing about this 4.1 percent GDP growth, right? Yet if you look at the statistics, real worker wages have continued to be flat for this period. The crisis itself was the greatest looting of the public purse in history. The crisis itself was a huge wealth transfer. The Obama administration should have forced a lot more recognition of the losses. These losses were real. They should have forced more loan write-downs. And recognition of the loss to the financial system. And they should have had a huge stimulus to offset the downdraft of recognizing those losses. And in fact the Japanese, early in their crisis, they said the biggest mistake we made was not writing down the bad loans in the banking system. Don't repeat our mistake.

And we did this in a more indirect manner by having the Fed engineer these super-low interest rates that were a transfer from savers to the financial system. Economist Ed Kane said that basically savers lost $300 billion in income a year. So that reduction of income right there, you see today. There's a Wall Street Journalstory about how pension funds are in crisis. There's not a single mention of the fact that the zero-interest-rate policies are the reason why the pensions are in distress. All retirees and long-term savers, life insurance, they're all in the same boat. It used to be that if you were a saver or an asset holder, you could get a decent positive return doing something not crazy. And the Fed took that away. The big reason the pensions are in crisis is because the way we dealt with the crisis.

We have this fallacy that normal people should be able to save for retirement. If public pension funds, which can invest at the very lowest possible fees, can't make this work, how is Joe Mom-and-Pop America gonna be able to do this? Again, it's back to the stagnant worker wages. So, great, we're not paying people enough, housing prices are very inflated. We've got this horrible medical system that costs way too much, and how are people supposed to put any money aside when their real estate and their rents and their health costs are going up?

Why do you think we have Trump? I mean, even though he did a big bait-and-switch, as we all know, there were a lot of people that lost their homes, their community wasn't what it used to be, particularly if they lived in the Rust Belt. And then you have these people on the coast saying, "Oh, they should go get training. It's disgusting." I mean, let them eat cake is let them get training. What you hear from these coastal elites: People over 40, even over 35, are basically non-hirable. Are you gonna train them? They're gonna waste their time thinking they can get a new job? I mean, that's just lunacy.

I think the Republicans, because they're sort of loud and proud, that's the way they behave, it's easier to point fingers at them. And in some sense they are more vocal proponents of bad ideology, but there's this great tendency in politics and in business to present whatever was done as being terrific and successful when it wasn't. This is one of my criticisms of the Obama administration, but now appears to be true of the Democratic Party generally, that they think the solution for every problem is better PR.

Photo: Tommaso Boddi/Getty Images

Photo: Tommaso Boddi/Getty Images

Boots Riley

Musician and filmmaker

The quote-unquote real-estate boom was all bullshit. One of the things that's in the movie — there's that billboard saying, "Be a responsible baby daddy, join Worry Free." Well, the way that the idea of buying a house was being sold, specifically to black people, was that you are being irresponsible with your money if you're not listening to the experts, and this is why black people are in poverty — they don't spend their money right. You should be buying a house. And that any other view was an irresponsible view! Because you're not listening to the experts — by the way, the experts are real-estate salespeople. To bring it up as this being a contradiction was to be thought of as some sort of conspiracy theorist. We haven't learned certain lessons. Some of us have — but the way we talk, the media thinks about things, we haven't learned certain lessons.

Photo: Daphne Borowski

Photo: Daphne Borowski

Steve Rattner

Financier

I think the job that was done by both the Bush administration and the Obama administration was really remarkable in retrospect. They were operating in real time, with banks literally close to failure over a weekend, banks having to be merged over a weekend to be saved. It's amazing to me in retrospect how many correct decisions both administrations made. I'm sure if they look back they would think of some things they might do differently. I suspect that if I looked at the auto thing, I might think of some things we should have done differently, but not many. So I think we should all be pretty grateful.

The key decision in the case of both the banking crisis and the auto crisis was the decision that government needed to step in. Remember, there were people who argued that the market should work and capitalism should be allowed to function and government had no business investing in banks or saving banks or saving auto companies. The pressure to not intervene was particularly acute during the Bush administration.

Astra Taylor

Activist

There's all this discussion about what happened, what went wrong, what led to 2016, and I'm always struck by the fact that the economic crisis is frequently left out of the narrative. Right? This right-wing resurgence we're seeing now also has its roots in the financial crisis. Because it's still running off this tea-party energy. I think 2008 is too often left out precisely because it does pose a tremendous challenge to the Democratic Establishment. Because then you have to look at the legacy of Bill Clinton and you have to examine Obama's handling of the bailout and the way he treated mortgage holders and the fact that there was not even a symbolic punishment of the people who had committed the crimes that left people absolutely devastated.

Paul Romer

Economist

Did you get a chance to look at this looting paper? This is a couple of crises ago. In effect, what [economist George Akerlof and I] showed is that seemingly small weaknesses in your regulatory system can open up enormous risks, and enormous opportunities for private profit. So what it tells you is that under-regulating or mis-regulating is much more dangerous than people generally accept. So I think most economists think of this as kind of, "We're on the top of a smooth hill. Even if you've got it kind of, sort of, right in terms of regulation, you're fine. A little deviation one side or the other, it won't really matter." We were trying to say, "No. It's like a cliff. You go a little bit over the cliff, in terms of what you allow with your regulatory system, you're gonna get really terrible outcomes."

Everybody disliked that paper. After the financial crisis, some people, including Larry Summers, told me they now saw that the looting story captured the reality in a way that they hadn't recognized before. This is what worries me, people are kind of heading back to the pre-crisis worldview. Regulation is never perfect. You can always kind of complain about imperfections. But I think the kind of weakening, at the behest of the industry, that we're going through right now should be generating a lot more academic concern than it is generating at the moment. There's a complacency that's setting back in. There's a tolerance now for, oh, maybe let's err a little bit on the side of under-regulating. You know, how much harm could it cause?

Stephanie Kelton

Economist

The knock-on effects that arose as a consequence of failing to keep people in their homes impact everything from academic performance of the kids who were in those families to the health of the parents, the balance sheets, the credit scores. When you lose your home and you lose your job, the aftereffects that stay with you make it difficult for tens of millions of Americans to even take advantage of the policies that were designed to bring about a recovery. Low interest rates, for example. Well, low interest rates don't help the unemployed person whose credit has been destroyed take advantage of cheaper borrowing, refinance a home when you've lost your home. The people who were unfortunate enough to have entered college around the time we were building up to the Great Recession, the early 2000s, 2004, 2005, you've likely taken out student loans to help cover the cost of college. Now you graduate and you enter into the labor market at the worst possible time in 35 years or whatever since the recession of the early 1980s. The prospects for finding employment at all are extremely grim, and then the jobs that you thought you would be competing for with advanced degrees and so forth aren't there. You're taking jobs that pay perhaps half of what you anticipated making. You can't pay off the student-loan debt and move out and start your life, so you stay home with your parents.

For that unfortunate cohort, there is a period of their lives, maybe it's ten years, where depressed earnings, a lack of ability to enter the job market, and so forth, it has lasting effects. That time period, that snapshot in time, that decade or so where they're going to suffer potentially a lifetime of damage as a consequence.

THE MARKET WAS REVEALED AS A CASINO

By Christopher Caldwell

Total U.S. household net worth dropped by $11.1 trillion in 2008.

The median income for 25-to-34-year-olds in America, $34,000, hasn't budged since 1977, adjusted for inflation.

Median household wealth collapsed.

2007: $126k

2016: $97k

The number of Americans worried about the economy multiplied nearly sixfold.

2007: 16 percent

2008: 86 percent

In 2016, the median wealth of a family headed by someone born in the 1980s was 34 percent below the level of earlier generations at the same 2007: age.

Mutual funds lost a third of their value: -38 percent.

The market value of all publicly traded companies was cut in half.

October 2007: $63 trillion

March 2009: $28.6 trillion

From 2005 to 2009, the median value of stocks and mutual funds owned by whites dropped by 9 percent.

The median value of holdings for African-Americans dropped by 71 percent (probably because of pressure to sell when prices were low).

Between 2007 and 2013, wages declined for the bottom 70 percent of all workers.

The retirement savings of black families fell by 35 percent from 2007 to 2010.

In a 2016 survey by the Fed, 28 percentof working-age adults said they had no retirement savings whatsoever.

The racial wealth gap, already large, ballooned.

Whites: $171k

Hispanics: $20.7k

African-Americans: $17.6k

In terms of household wealth, every group suffered — but some more than others.

Hispanics: -66 percent

Asian-Americans: -54 percent

African-Americans: -53 percent

Whites: -16 percent

Consumer credit-card debt at the end of 2017 was over $1 trillion (about 30% higher than in 2008).

Millennials have taken on at least 300 percent more student-loan debt than their parents' generation.

The unemployed took many more weeks to find work.

May 2008: 7.9

June 2010: 25.2

In a December 2017 poll by YouGov, 38 percent of those surveyed said they didn't know when they'd be debt-free. 30 percent of respondents thought they'd never be out of debt.

63 percent of Americans say they don't have enough money in savings to cover a $500 health-care expense.

In 2017, women had nearly 500,000 fewer babies than in 2007, although there were 7 percent more women of prime childbearing age.

The suicide rate rose 4 percent from 1999 to 2010: 4,750 additional deaths.

24 million adult millennials, or 32 percent, still live at home.

79 million Americans live in a "shared household" with at least one extra, nonfamily resident.

More college grads moved in with their parents.

2005: 19 percent

2016: 28 percent

As of 2017, only 34.2 percent of homes have recovered their value from before the recession. (Still below 2008 value.)

From 2000 to 2015, homeownership declined in 90% of all U.S. metropolitan areas.

Reporting by Joy Crane and Matt Stieb

WTF HAPPENED?

Sheila Bair

Former head of FDIC

Once the system was stabilized in early 2009, we had an opportunity to restructure and break up Citigroup in particular, but we didn't do that. I think that was a missed opportunity. We just reinforced too-big-to-fail with all these bailouts, let's face it. Other than Lehman Brothers, nobody took their medicine. Restructuring Citigroup would have sent a powerful signal that the government had the gumption and courage to stand up to these very large institutions, and to impose losses on bond holders.

I think we've improved the system on the margin. There are higher capital requirements, there's better bank liquidity, less reliance on short-term financing, less reliance on debt among the regulated banks. Those are all positive things. But the financial system we have is still basically the financial system we had in 2008, with more capital and less reliance on short-term funding, so whether it's enough? I hope it is.

I wish we had more Republicans who would stand up to these cronies who want the government bailouts. I think a lot of people still want that on Wall Street — it's secretly what they want. They think it's the government's obligation to keep them afloat. I'm a capitalist, and I'd rather have the state own them than have that system.

It's very frustrating. It's just stupid economics. Set the morality aside; it's just dumb economics to have a system like this where you're propping up inefficient, bloated institutions. So there are good economic reasons to not have the system we had in 2008, and whether we've gotten rid of it or not I don't know. I think we won't know until a big bank gets in trouble again. Then we'll see what happens. I don't even want to think about what the political fallout would be.

Corey Robin

Political theorist

The first and most obvious fallout is that in the '90s and the '80s — when pensions were being switched over to 401(k)s — there was a strong sense that the stock market really was this kind of profound divination and assurance of all well-being. You've got a whole generation of people, my generation and even a little bit older, whose entire futures are caught up in — if they're lucky, by the way — 401(k)s and the state of the stock market. It really knocked the wind out of the fundamental belief that the market would take care of things.

A couple weeks ago, a friend on Facebook who's in advertising — and who's not a political person at all — posted something: Hey, guys, what are we all thinking about retirement? And it was just shocking, the unanimity among everybody, that retirement was not something that would ever happen. And these are people who are upper-middle class, professional managerial class, and not thinking of working forever because work is fun.

The triumph of the neoliberal consensus, post-1989, was to naturalize the economy. Here are these laws that are fairly apolitical, untouchable, the equivalent of the laws of nature. What the financial crisis, and then the response to the financial crisis, did was to denaturalize that again. So suddenly the economy looks political. The combination of the stimulus package and Obamacare threw open all over again the possibility of government intervention in the economy in a way that had seemed very much closed off, permanently, for a generation. But while [the stimulus package and other measures] restored some kind of basic semblance of health in the economy, all of the fundamentals about wages in particular remained pretty much the same. Our economic situation as a lived experience has not changed and is as fundamentally precarious as it was before. And that's a very explosive situation.

You know, Tocqueville has this very famous argument in his book on the French Revolution, where he says it's not steady immiseration that creates the conditions for revolution. It's actually situations that are kind of getting better but not getting better fast enough. That's when people start looking at more radical alternatives.

Robert Shiller

Economist

I was in a panel around 2005 when an economist from Freddie Mac said that they do stress tests and they're safe. I was raising the possibility that home prices might fall. He said, "We have taken simulations that go as far as a 13 percent drop in home prices, and we can survive that." I'm paraphrasing him.

So then I said, "Well, what if it falls more than 13 percent?" And he said, "They've never fallen more than that, not since the Great Depression." And so I said, "Well, what about that? It happened in the Great Depression." He sort of made me look like a fool for saying that could happen. So these things become so remote that they become storybook-land, and then we set ourselves up for another one.

People learn things — sort of — and then years go by, and there are new success stories that people hear about and they want to be part of it. And then people who warn them about getting overexposed, as more years go by, start to look like losers.

One thing that has brought back some of the old feeling is the fact that we've set new records for home prices in nominal terms and the stock market, so it provides some sense of vindication for those feelings of ten years ago. We've had three big peaks. One was in the year 2000 in the stock market, and then in 2007 in the stock market and the housing market. And then now again, both the stock market and the housing market are at record highs. So the sense of humiliation is fading, and the sense that the 2000s, before 2007, was a mistake is fading.

I don't think that we can protect people from human nature. We have a stock market, which is on its own. Way back in the 1930s, they put on margin requirements to prevent you from borrowing too much to buy stock, but that didn't stop us. And so you plug holes, and then it's like the Dutch boy and the dike. Another one springs because there's a basic human drive, a speculative drive. So to some extent we have to let people make their own mistakes. Along the way a lot of great things happen.

Matt Bruenig

Policy analyst

The main legacy of the Great Recession is going to be accelerating the concentration of wealth. I have a figure that's going to come out in our next report that says between 2007 and 2016, the average wealth of the top one percent increased by $4.9 million at the same time as the wealth of the median family declined by $42,000. The wealth is being sucked out of the middle and pushed to the top. That's what you would expect from the type of bailout that they did. They let homeowners drown and they bailed out financial institutions whose shareholders are mostly very affluent families.

Young people who came into working age, they face permanent repercussions because they can't get jobs, or if they can get jobs, the jobs are not paying that well. And of course a lot of them are putting on more and more debt if they're getting a college education.

And so you kind of get a lost generation of sorts. A mild lost generation. You know, like they weren't killed in a war. And one of the ways that you see this effect is a drop in fertility. There was a very marked decline after the recession. And that's mostly young adults who obviously are making an economic decision that they can't afford children. And you don't recover from that.

And obviously there's a racial component too that I feel has been very overlooked. I don't think people realize just how bad the Great Recession was for black and Latino families. The level of wealth decline in those groups … You could write a whole reparations article just off what happened in the past eight years. Like, you don't even need to go back to the GI Bill. You could just say, "Look at what happened where clearly racially predatory bankers load black families up with these subprime mortgages and just extract wealth out of them." That's the story that's not been fully discussed, for one reason or another.

Yves Smith

Founder, naked capitalism

Trump is crowing about this 4.1 percent GDP growth, right? Yet if you look at the statistics, real worker wages have continued to be flat for this period. The crisis itself was the greatest looting of the public purse in history. The crisis itself was a huge wealth transfer. The Obama administration should have forced a lot more recognition of the losses. These losses were real. They should have forced more loan write-downs. And recognition of the loss to the financial system. And they should have had a huge stimulus to offset the downdraft of recognizing those losses. And in fact the Japanese, early in their crisis, they said the biggest mistake we made was not writing down the bad loans in the banking system. Don't repeat our mistake.

And we did this in a more indirect manner by having the Fed engineer these super-low interest rates that were a transfer from savers to the financial system. Economist Ed Kane said that basically savers lost $300 billion in income a year. So that reduction of income right there, you see today. There's a Wall Street Journalstory about how pension funds are in crisis. There's not a single mention of the fact that the zero-interest-rate policies are the reason why the pensions are in distress. All retirees and long-term savers, life insurance, they're all in the same boat. It used to be that if you were a saver or an asset holder, you could get a decent positive return doing something not crazy. And the Fed took that away. The big reason the pensions are in crisis is because the way we dealt with the crisis.

We have this fallacy that normal people should be able to save for retirement. If public pension funds, which can invest at the very lowest possible fees, can't make this work, how is Joe Mom-and-Pop America gonna be able to do this? Again, it's back to the stagnant worker wages. So, great, we're not paying people enough, housing prices are very inflated. We've got this horrible medical system that costs way too much, and how are people supposed to put any money aside when their real estate and their rents and their health costs are going up?

Why do you think we have Trump? I mean, even though he did a big bait-and-switch, as we all know, there were a lot of people that lost their homes, their community wasn't what it used to be, particularly if they lived in the Rust Belt. And then you have these people on the coast saying, "Oh, they should go get training. It's disgusting." I mean, let them eat cake is let them get training. What you hear from these coastal elites: People over 40, even over 35, are basically non-hirable. Are you gonna train them? They're gonna waste their time thinking they can get a new job? I mean, that's just lunacy.

I think the Republicans, because they're sort of loud and proud, that's the way they behave, it's easier to point fingers at them. And in some sense they are more vocal proponents of bad ideology, but there's this great tendency in politics and in business to present whatever was done as being terrific and successful when it wasn't. This is one of my criticisms of the Obama administration, but now appears to be true of the Democratic Party generally, that they think the solution for every problem is better PR.

Photo: Tommaso Boddi/Getty ImagesBoots Riley

Musician and filmmaker

The quote-unquote real-estate boom was all bullshit. One of the things that's in the movie — there's that billboard saying, "Be a responsible baby daddy, join Worry Free." Well, the way that the idea of buying a house was being sold, specifically to black people, was that you are being irresponsible with your money if you're not listening to the experts, and this is why black people are in poverty — they don't spend their money right. You should be buying a house. And that any other view was an irresponsible view! Because you're not listening to the experts — by the way, the experts are real-estate salespeople. To bring it up as this being a contradiction was to be thought of as some sort of conspiracy theorist. We haven't learned certain lessons. Some of us have — but the way we talk, the media thinks about things, we haven't learned certain lessons.

Photo: Daphne BorowskiSteve Rattner

Financier

I think the job that was done by both the Bush administration and the Obama administration was really remarkable in retrospect. They were operating in real time, with banks literally close to failure over a weekend, banks having to be merged over a weekend to be saved. It's amazing to me in retrospect how many correct decisions both administrations made. I'm sure if they look back they would think of some things they might do differently. I suspect that if I looked at the auto thing, I might think of some things we should have done differently, but not many. So I think we should all be pretty grateful.

The key decision in the case of both the banking crisis and the auto crisis was the decision that government needed to step in. Remember, there were people who argued that the market should work and capitalism should be allowed to function and government had no business investing in banks or saving banks or saving auto companies. The pressure to not intervene was particularly acute during the Bush administration.

Astra Taylor

Activist

There's all this discussion about what happened, what went wrong, what led to 2016, and I'm always struck by the fact that the economic crisis is frequently left out of the narrative. Right? This right-wing resurgence we're seeing now also has its roots in the financial crisis. Because it's still running off this tea-party energy. I think 2008 is too often left out precisely because it does pose a tremendous challenge to the Democratic Establishment. Because then you have to look at the legacy of Bill Clinton and you have to examine Obama's handling of the bailout and the way he treated mortgage holders and the fact that there was not even a symbolic punishment of the people who had committed the crimes that left people absolutely devastated.

Paul Romer

Economist

Did you get a chance to look at this looting paper? This is a couple of crises ago. In effect, what [economist George Akerlof and I] showed is that seemingly small weaknesses in your regulatory system can open up enormous risks, and enormous opportunities for private profit. So what it tells you is that under-regulating or mis-regulating is much more dangerous than people generally accept. So I think most economists think of this as kind of, "We're on the top of a smooth hill. Even if you've got it kind of, sort of, right in terms of regulation, you're fine. A little deviation one side or the other, it won't really matter." We were trying to say, "No. It's like a cliff. You go a little bit over the cliff, in terms of what you allow with your regulatory system, you're gonna get really terrible outcomes."

Everybody disliked that paper. After the financial crisis, some people, including Larry Summers, told me they now saw that the looting story captured the reality in a way that they hadn't recognized before. This is what worries me, people are kind of heading back to the pre-crisis worldview. Regulation is never perfect. You can always kind of complain about imperfections. But I think the kind of weakening, at the behest of the industry, that we're going through right now should be generating a lot more academic concern than it is generating at the moment. There's a complacency that's setting back in. There's a tolerance now for, oh, maybe let's err a little bit on the side of under-regulating. You know, how much harm could it cause?

Stephanie Kelton

Economist

The knock-on effects that arose as a consequence of failing to keep people in their homes impact everything from academic performance of the kids who were in those families to the health of the parents, the balance sheets, the credit scores. When you lose your home and you lose your job, the aftereffects that stay with you make it difficult for tens of millions of Americans to even take advantage of the policies that were designed to bring about a recovery. Low interest rates, for example. Well, low interest rates don't help the unemployed person whose credit has been destroyed take advantage of cheaper borrowing, refinance a home when you've lost your home. The people who were unfortunate enough to have entered college around the time we were building up to the Great Recession, the early 2000s, 2004, 2005, you've likely taken out student loans to help cover the cost of college. Now you graduate and you enter into the labor market at the worst possible time in 35 years or whatever since the recession of the early 1980s. The prospects for finding employment at all are extremely grim, and then the jobs that you thought you would be competing for with advanced degrees and so forth aren't there. You're taking jobs that pay perhaps half of what you anticipated making. You can't pay off the student-loan debt and move out and start your life, so you stay home with your parents.

For that unfortunate cohort, there is a period of their lives, maybe it's ten years, where depressed earnings, a lack of ability to enter the job market, and so forth, it has lasting effects. That time period, that snapshot in time, that decade or so where they're going to suffer potentially a lifetime of damage as a consequence.

THE MARKET WAS REVEALED AS A CASINO

By Christopher Caldwell

Brazil, September 15, 2008. Photo: Mauricio Lima/AFP/Getty Images

The quarter-century leading up to the crash was a golden age not just of financial gambling but of gambling more generally. Until the election of Ronald Reagan in 1980, playing the ponies or numbers had in many places been a vice and playing the slots a crime. Casinos and sports betting were banned everywhere but Nevada and Atlantic City. By 2008, gambling was a hundred-billion-dollar industry touching every state except Utah and Hawaii. Riverboat gambling was reestablished, especially in the Midwest. Indian tribes opened gambling resorts in 29 states. Vast regional and national lotteries flourished alongside state ones.

Gambling was in the Spirit of the Age. The expression "casino capitalism" came into vogue. But what did it actually mean?

Partly it had to do with an erosion of character. The rewards of capitalism had, in the public mind, come unbundled from the set of virtues once called the Protestant work ethic. Getting rich had as much to do with luck or effrontery as sustained effort.

Partly it had to do with irresponsibility. "Derivatives" had always existed as ways to hedge risk, as a sort of insurance. But new, mathematically complex "exotic" derivatives were risk itself. Their prices were not transparent — one model for putting a value on them was called a "Monte Carlo simulation."

Right up until the early fall of 2008, many Americans had been comfortable with the notion that a well-functioning economy looked a good deal like a well-functioning casino. No longer. Today, they're furious at the house.

THE CENTER COLLAPSED, BUT A NEW UTOPIANISMFOLLOWED

By Timothy Shenk

The quarter-century leading up to the crash was a golden age not just of financial gambling but of gambling more generally. Until the election of Ronald Reagan in 1980, playing the ponies or numbers had in many places been a vice and playing the slots a crime. Casinos and sports betting were banned everywhere but Nevada and Atlantic City. By 2008, gambling was a hundred-billion-dollar industry touching every state except Utah and Hawaii. Riverboat gambling was reestablished, especially in the Midwest. Indian tribes opened gambling resorts in 29 states. Vast regional and national lotteries flourished alongside state ones.

Gambling was in the Spirit of the Age. The expression "casino capitalism" came into vogue. But what did it actually mean?

Partly it had to do with an erosion of character. The rewards of capitalism had, in the public mind, come unbundled from the set of virtues once called the Protestant work ethic. Getting rich had as much to do with luck or effrontery as sustained effort.

Partly it had to do with irresponsibility. "Derivatives" had always existed as ways to hedge risk, as a sort of insurance. But new, mathematically complex "exotic" derivatives were risk itself. Their prices were not transparent — one model for putting a value on them was called a "Monte Carlo simulation."

Right up until the early fall of 2008, many Americans had been comfortable with the notion that a well-functioning economy looked a good deal like a well-functioning casino. No longer. Today, they're furious at the house.

THE CENTER COLLAPSED, BUT A NEW UTOPIANISMFOLLOWED

By Timothy Shenk

China, September 16, 2008. Photo: China Photos/Getty Images

During the financial crisis, the most important lie that political elites told themselves was that they had no other option. (As Ben Bernanke explained to congressional leaders when arguing for the Wall Street bailout, "If we don't do this, we may not have an economy on Monday.") But after a decade of populist revolts, no longer are policy-makers dancing on the head of a pin, seeking the right balance between global markets and technocratic nudging. The crash was an act of creative destruction, and the once unimaginable is now the stuff of cable-news roundtables.

On the left, Democrats are debating Medicare for all, tuition-free college, and a federal jobs guarantee. On the right, Fox News is fulminating over the deep state and conservative intellectuals are mainstreaming the case for repealing birthright citizenship. All this is taking place while unemployment is hovering around 4 percent and economic growth is steady. Does anyone want to guess what will happen when the good times stop?

The future is wide open, wider than it's been than at any time since the Great Depression. If the difference between Mitt Romney and Barack Obama seemed vast in 2012, imagine what will happen when the generation of Stephen Miller and Alexandria Ocasio-Cortez takes power. For all their differences, Miller and Ocasio-Cortez both demonstrate the central lesson from the last decade of crisis: There is always another option. The question is whether we will choose a better one.

A GLOSSARY OF THE GREAT RECESSION

The One Percent

The crash didn't invent inequality, of course; it had been booming for decades.

But sometimes you only recognize something when you have a name for it. How did we ever talk about the economy before?

Kickstarter, GoFundMe, Patreon

When did we give up hope that the market would provide us with the things we cherished most, from art to entrepreneurship to health care? In retrospect, the answer seems obvious.

Bitcoin

How could you even trust the Fed anymore? The older folks hoovered up gold, which basically doubled in value in the four years after the crash. Younger folks dove into cryptocurrency; bitcoin, the first, was registered as a domain in August 2008.

Do You Really Know What Bitcoin Is?

Here, our super-simplified explanation — and what to know about the cryptocraze roller coaster.

"Recovery"

When you have the longest continuous period of economic growth in American history and nobody notices, there might be a problem with your terms. The problem was, the recovery was also the slowest.

China

Maybe Americans would've been a little more satisfied about the anemic recovery, and a little less terrified about what it meant for the country's superpower status, if China's growth didn't bottom out at 6 percent (in 2009, when the U.S. was at -3.5 percent) and then quickly recover to north of 12 percent one year later. (Oh, and it's basically building all new infrastructure in Africa and South America, its Belt-and-Road initiative like a Suez Canal project on imperial steroids.)

Tea Party

At the time, liberals dismissed the protest cosplay as "Astroturfing." But so what if it was paid for by the Kochs? Maybe that's how it was able to take over a political party, and then the government.

Occupy

It felt like a revolution, for a minute at least.

Twilight of the Elites

MSNBC host Chris Hayes's 2012 book named the metanarrative of the era: Trust in authorities and Establishment institutions was in decline well before the crash, but the crisis (and its aftermath) only accelerated the collapse of faith.

Survivalism

What do the elites do in the twilight? Retreat to their end-of-the-world bunkers, behind their electrified fences, on their New Zealand estates. Those who can't afford that kind of disaster prep could at least grow some gnarly beards and pack a go-bag.

Adult Children Living With Their Parents

This is what the non-elites did, enough of them to make it a meme, anyway.

Gaming

In 2016, economist Erik Hurst proposed that so many young men were missing from the workforce because they were choosing to spend their days playing video games instead. The data didn't exactly hold up, but the image is hard to shake.

Peak TV

How those of us not into World of Warcraft choose to escape the real world.

The Business of Too Much TV

There are more great shows in production now than ever before — but it's never been harder to make one.

Wellness

If you couldn't save the world, at least you could preserve your own body. Your skin especially. Which was important, because the ambient anxiety takes a toll.

Instagram

Probably not an accident that the representative social-media platform of the past decade is powered by envy.

The Death of News

It began with Craigslist killing classified revenue, but the death of American newspapers rapidly accelerated after 2008 — the number of jobs in the industry falling from about 350,000 before the crash to well under 200,000 today.

The Gig Economy

The numbers say there are actually fewer people working "contingent jobs" than before the crash, as hard as that may be to believe (3.8 percent of workers, according to the Bureau of Labor Statistics, down from 4.1 percent in 2005).

Presumably the term stuck, anyway, in part because it was suddenly being sold to us as the future of work by billionaire venture capitalists ("Get Your Side Hustle On!" — Uber). More importantly, because suddenly, and by comparison, anyone outside of the one percent felt extremely "contingent."

The Sharing Economy

Why own anything when you could just rent it? In an earlier era, this would not have seemed a wise question.

Millennials

As the decade has worn on, every single aspect of the generational stereotype — the narcissism, the self-salesmanship, the earnestness and the entrepreneurship — looks less like a feature of coddled youth and something more like its opposite: the survival instincts of a desperate generation with nothing to sell but themselves.

"Globalists"

We live now in a nation so saturated in conspiracy theory the paranoia has seeped into the real world: Pizzagate, QAnon, a president who might be a puppet. How did this happen? "The internet" is one conventional answer, but a more compelling one might be the financial crisis — a classic paranoid fantasy, in which the world's bankers stockpile profits from bets whose downsides would be shouldered by workers and, in the moment of reckoning, with the global economy collapsed, escape not just unprosecuted but protected by the powers of governments eager to serve their needs. To explain it, Alex Jones posted his first YouTube video that very same year; Glenn Beck moved to Fox News in 2009.

What If Trump Has Been a Russian Asset Since 1987?

A plausible theory of mind-boggling collusion.

Iraq

The country elected an antiwar president in 2008, but what it got, instead, was an anti-recession one. There are, of course, many ugly reasons that Americans began looking away from the wars being fought in their names after almost a decade of struggle, failure, and death overseas. But a crisis at home surely contributed, too.

"Precariat"

We didn't have a word to describe just how fragile a white-collar professional could feel in the midst of a steadily growing economy with low unemployment, probably because never before had it seemed reasonable that that could even be a thing. The word doesn't exactly roll off the tongue, but at least we have one now.

Joe the Plumber

Yeah, that guy was definitely a worthy adversary to Obama on pocketbook issues.

R>G

In 2014, French economist Thomas Piketty became the nerdiest rock star in the world. In Capital in the Twenty-First Century, he introduced a small equation, backed up by years of quantitative research, claiming to show exactly why global inequality was growing. He demonstrated that as long as the return on capital (r) exceeded the growth rate of the economy (g), the one percent would take more and more of the pie. Soon you could buy "r>g" on a T-shirt.

SoundCloud Rap

Despair has never been a bigger part of pop music than it is right now, and we have a generation of rappers for whom weed and coke have been replaced as mascot drugs by fear-numbing Xanax.

How to Tell All the SoundCloud Rappers Apart

From the face tattoos to the crimes to their confusingly similar names, we've got you covered.

Artisanal Everything

If the world came to an end, one could survive, particularly if one were a somewhat well-off young white person, by pickling everything in sight and retreating to simpler times. In the horror movie A Quiet Place, a Brooklyn-esque family must tiptoe around their upstate farmhouse so as not to be devoured by monsters with great hearing (but the place also looks like it might go for $350 a night on Airbnb in the summer months).

Mitch McConnell

The belt-tightening extended to politics, too — and as a zero-sum perspective took over Congress, everything got very dog-eat-dog. A win for one side became a loss for the other, which meant that, in a period of divided government, absolutely nothing would ever get done.

Austerity

In Europe, the word had a weaponized meaning: that, almost exactly as Naomi Klein predicted in The Shock Doctrine, faced with a crisis, any crisis, the world's bankers and governments would together put the needs of capital first, making giant cuts to spending even in the midst of five-year-long recessions and 25 percent unemployment rates. In the United States, there weren't real cuts — though the stimulus wasn't as large as some might have liked — and so the word conjured less a policy prerogative than a national mood. There just didn't seem to be any money around, in Washington especially, and little hope, after the tea party swept into Congress in 2010, of accomplishing anything of any scale.

Bailout

What you called government aid someone else got — the banks, the auto business, Fannie Mae and Freddie Mac.

The One Jailed Wall Street Banker

Yep, there was just one — an Egyptian-born trader named Kareem Serageldin.

Zombie Apocalypse

It's the only kind you can market in a zombie economy.

The Dark Knight Rises

Supervillain (and bank robber) Bane gives an Occupy-like speech outside a prison.

MMT

If the global financial crisis was our Great Depression, didn't we need our own Keynesianism? Modern monetary theory, a formulation of demand-side economics that suggests governments can print as much money as is necessary for expenditures and need to tax citizens only in order to keep inflation down, seemed closest, with its appealing contrarianism (and promise of expansive government stimuli).

The 47 Percent

Would anyone have believed, before the crash, that just about half the country was on the dole? Romney's gaffe certainly had more of an audience in the age of the Obama phone.

Populism

In Europe, centrist governments turned to austerity, which left victims of the crisis in even worse shape — in some cases — and created an opening for Trump-style extreme-right nativists. In the Netherlands, Geert Wilders, of the Party for Freedom, tweets about countries like his becoming "retarded Islamic Sharia-nations." In France, Marine Le Pen — daughter of the infamous Holocaust denier — has made the near-fascist National Front a major contender. Alternative for Germany, which aims to ban mosques, is now that country's largest opposition group.

Alt-right

What happens when the core ideology of the Western right fails on a global scale? You get an alternative: a loose coalition of right-wing ideologies, indifferent at best to capitalism, focused intently on racial nationalism, traditional gender roles, and violent enforcement of state sovereignty. Also, for some reason, a cartoon frog called Pepe? Was that how they were able to take over the White House?

Beyond Alt: Understanding the New Far Right

Coming to grips with the most potent political movement of our age.

Incels

Way back in the 1990s, French novelist Michel Houellebecq had suggested that a truly liberated sexual marketplace would work just the way any other unregulated capitalist system would — delivering the lion's share of the goods, in this case sex, to the few, while the many languished in resentment. Apparently, the problem gets more acute when the economy crashes and the sexless become jobless, too.

The Elephant Chart

Capitalism may have failed you, economist Branko Milanovic's iconic graph said, but it was still working for the people in the world who needed it most: Tracing income growth for every global percentile, the chart showed great gains for most of the world's poor, stagnation and loss for the middle class of the First World, and huge gains again for the top one percent (the global rich). Fairly or unfairly, those gains for Vietnam's workers were seen as losses for American workers in the new global economy.

Summer of Scam

When the economy looks like a grift, and the president and his henchmen hustlers too, you'd be foolish not to get yours where you can, whether you're a fake German heiress or a Steve Jobs wannabe with a chemistry set.

How an Aspiring 'It' Girl Tricked New York's Party People — and Its Banks

Somebody had to foot the bill for Anna Delvey's fabulous new life. The city was full of marks.

HGTV

The metanarrative of every house-flipping show is that shiplap and a farm sink can restore the boom years, one foreclosure at a time.

HGTV Is a Never-ending Fantasy Loop. Look Deeper, and It Gets Pretty Ugly.

There's nothing more addictively soothing than watching someone flipping homes on HGTV. Until we end up in a real-life rerun of the housing bubble.

The App Store

The ten years before 2008 were a remarkable period of tech development, culminating in the defining gadget of the 21st century, the iPhone. We basically haven't gotten anything good since; an apt symbol for the era's tech boom may be found in "Yo," the app that sends the phrase "Yo!" — and only the phrase "Yo!" — to your friends.

The End of Growth

In 2016, economist Robert Gordon proposed a radical rethinking of economic history: The rapid rise in standard of living between 1870 and 1970 may have been a historical anomaly, unprecedented and unlikely to ever be repeated.

MEN FELT PUNISHED

By Hanna Rosin

When, in 2012, I titled my book The End of Men, I did it partly for effect. My argument was true enough, that the 2008 recession had destroyed a certain model of manhood, made it obvious that for white working-class men it was becoming impossible to skip a college degree and live a comfortable middle-class life.

But predicting cultural upheavals from economic shifts is always dicey. Would men and women really start to relate to each other differently? Would American manhood collapse into a victim identity — and each private demise collect into a tornado of public rage? As economic forecasters will tell you, human beings tend to surprise.

Well, in this case they didn't. We've arguably recovered from the Great Recession, with one glaring exception: Nearly one in five men between the ages of 25 and 54 with a high-school degree or less aren't in the workforce and aren't looking for work. And it's particularly American: In the U.K., working-class men bounced back along with everyone else.

Weirdly, we don't really know why a certain sector of American men put up the white flag around 2008. Logical homo economicus would have adjusted to the new economy, trained for the growing number of jobs in the service industry, health care, government; he would've accepted an easing of strict gender roles in family life. Homo americanus basically said screw that feminized bullshit — and resurrected a cartoon version of brute machismo with a twist of victimhood.

In the corners of the internet where the new aggrieved men find solace, what flourishes is the stubborn logic of biological imperative: Men and women aren't supposed to change because their roles are set by nature. The only fix is for women to return to what they were intended for. It was Donald Trump's genius to recognize early on that these white men were a separate and unified interest group, and his luck that he so instinctively speaks their language.

It's ironic that the end-of-men era opened a space for an already-ended man to take power, but not shocking. Periods of gender backlash always have the drama of war. Recently, women have brought down powerful men in ways that were unimaginable only a few years ago. And recently, men have wielded power around the world in ways that were unimaginable only a few years ago. It's hard to identify a clear trend, but to me all doesn't seem lost. I can more easily imagine a female president post-Trump than pre-.

What does disturb me is what's happening on the ground. I keep in touch with some men from my book, and what I've noticed lately in their voices is a deep, multilayered suspicion of all female-kind. Their private experiences with the women in their lives have gotten folded into a readily available narrative about how modern womanhood has failed America. And, as with all grand victim narratives, it's hardening into an unassailable truth.

During the financial crisis, the most important lie that political elites told themselves was that they had no other option. (As Ben Bernanke explained to congressional leaders when arguing for the Wall Street bailout, "If we don't do this, we may not have an economy on Monday.") But after a decade of populist revolts, no longer are policy-makers dancing on the head of a pin, seeking the right balance between global markets and technocratic nudging. The crash was an act of creative destruction, and the once unimaginable is now the stuff of cable-news roundtables.

On the left, Democrats are debating Medicare for all, tuition-free college, and a federal jobs guarantee. On the right, Fox News is fulminating over the deep state and conservative intellectuals are mainstreaming the case for repealing birthright citizenship. All this is taking place while unemployment is hovering around 4 percent and economic growth is steady. Does anyone want to guess what will happen when the good times stop?

The future is wide open, wider than it's been than at any time since the Great Depression. If the difference between Mitt Romney and Barack Obama seemed vast in 2012, imagine what will happen when the generation of Stephen Miller and Alexandria Ocasio-Cortez takes power. For all their differences, Miller and Ocasio-Cortez both demonstrate the central lesson from the last decade of crisis: There is always another option. The question is whether we will choose a better one.

A GLOSSARY OF THE GREAT RECESSION

The One Percent

The crash didn't invent inequality, of course; it had been booming for decades.

But sometimes you only recognize something when you have a name for it. How did we ever talk about the economy before?

Kickstarter, GoFundMe, Patreon

When did we give up hope that the market would provide us with the things we cherished most, from art to entrepreneurship to health care? In retrospect, the answer seems obvious.

Bitcoin

How could you even trust the Fed anymore? The older folks hoovered up gold, which basically doubled in value in the four years after the crash. Younger folks dove into cryptocurrency; bitcoin, the first, was registered as a domain in August 2008.

Do You Really Know What Bitcoin Is?

Here, our super-simplified explanation — and what to know about the cryptocraze roller coaster.

"Recovery"

When you have the longest continuous period of economic growth in American history and nobody notices, there might be a problem with your terms. The problem was, the recovery was also the slowest.

China

Maybe Americans would've been a little more satisfied about the anemic recovery, and a little less terrified about what it meant for the country's superpower status, if China's growth didn't bottom out at 6 percent (in 2009, when the U.S. was at -3.5 percent) and then quickly recover to north of 12 percent one year later. (Oh, and it's basically building all new infrastructure in Africa and South America, its Belt-and-Road initiative like a Suez Canal project on imperial steroids.)

Tea Party

At the time, liberals dismissed the protest cosplay as "Astroturfing." But so what if it was paid for by the Kochs? Maybe that's how it was able to take over a political party, and then the government.

Occupy

It felt like a revolution, for a minute at least.

Twilight of the Elites

MSNBC host Chris Hayes's 2012 book named the metanarrative of the era: Trust in authorities and Establishment institutions was in decline well before the crash, but the crisis (and its aftermath) only accelerated the collapse of faith.

Survivalism

What do the elites do in the twilight? Retreat to their end-of-the-world bunkers, behind their electrified fences, on their New Zealand estates. Those who can't afford that kind of disaster prep could at least grow some gnarly beards and pack a go-bag.

Adult Children Living With Their Parents

This is what the non-elites did, enough of them to make it a meme, anyway.

Gaming

In 2016, economist Erik Hurst proposed that so many young men were missing from the workforce because they were choosing to spend their days playing video games instead. The data didn't exactly hold up, but the image is hard to shake.

Peak TV

How those of us not into World of Warcraft choose to escape the real world.

The Business of Too Much TV

There are more great shows in production now than ever before — but it's never been harder to make one.

Wellness

If you couldn't save the world, at least you could preserve your own body. Your skin especially. Which was important, because the ambient anxiety takes a toll.

Probably not an accident that the representative social-media platform of the past decade is powered by envy.

The Death of News

It began with Craigslist killing classified revenue, but the death of American newspapers rapidly accelerated after 2008 — the number of jobs in the industry falling from about 350,000 before the crash to well under 200,000 today.

The Gig Economy

The numbers say there are actually fewer people working "contingent jobs" than before the crash, as hard as that may be to believe (3.8 percent of workers, according to the Bureau of Labor Statistics, down from 4.1 percent in 2005).

Presumably the term stuck, anyway, in part because it was suddenly being sold to us as the future of work by billionaire venture capitalists ("Get Your Side Hustle On!" — Uber). More importantly, because suddenly, and by comparison, anyone outside of the one percent felt extremely "contingent."

The Sharing Economy

Why own anything when you could just rent it? In an earlier era, this would not have seemed a wise question.

Millennials

As the decade has worn on, every single aspect of the generational stereotype — the narcissism, the self-salesmanship, the earnestness and the entrepreneurship — looks less like a feature of coddled youth and something more like its opposite: the survival instincts of a desperate generation with nothing to sell but themselves.

"Globalists"

We live now in a nation so saturated in conspiracy theory the paranoia has seeped into the real world: Pizzagate, QAnon, a president who might be a puppet. How did this happen? "The internet" is one conventional answer, but a more compelling one might be the financial crisis — a classic paranoid fantasy, in which the world's bankers stockpile profits from bets whose downsides would be shouldered by workers and, in the moment of reckoning, with the global economy collapsed, escape not just unprosecuted but protected by the powers of governments eager to serve their needs. To explain it, Alex Jones posted his first YouTube video that very same year; Glenn Beck moved to Fox News in 2009.

What If Trump Has Been a Russian Asset Since 1987?

A plausible theory of mind-boggling collusion.

Iraq

The country elected an antiwar president in 2008, but what it got, instead, was an anti-recession one. There are, of course, many ugly reasons that Americans began looking away from the wars being fought in their names after almost a decade of struggle, failure, and death overseas. But a crisis at home surely contributed, too.

"Precariat"

We didn't have a word to describe just how fragile a white-collar professional could feel in the midst of a steadily growing economy with low unemployment, probably because never before had it seemed reasonable that that could even be a thing. The word doesn't exactly roll off the tongue, but at least we have one now.

Joe the Plumber

Yeah, that guy was definitely a worthy adversary to Obama on pocketbook issues.

R>G

In 2014, French economist Thomas Piketty became the nerdiest rock star in the world. In Capital in the Twenty-First Century, he introduced a small equation, backed up by years of quantitative research, claiming to show exactly why global inequality was growing. He demonstrated that as long as the return on capital (r) exceeded the growth rate of the economy (g), the one percent would take more and more of the pie. Soon you could buy "r>g" on a T-shirt.

SoundCloud Rap

Despair has never been a bigger part of pop music than it is right now, and we have a generation of rappers for whom weed and coke have been replaced as mascot drugs by fear-numbing Xanax.

How to Tell All the SoundCloud Rappers Apart

From the face tattoos to the crimes to their confusingly similar names, we've got you covered.

Artisanal Everything

If the world came to an end, one could survive, particularly if one were a somewhat well-off young white person, by pickling everything in sight and retreating to simpler times. In the horror movie A Quiet Place, a Brooklyn-esque family must tiptoe around their upstate farmhouse so as not to be devoured by monsters with great hearing (but the place also looks like it might go for $350 a night on Airbnb in the summer months).

Mitch McConnell

The belt-tightening extended to politics, too — and as a zero-sum perspective took over Congress, everything got very dog-eat-dog. A win for one side became a loss for the other, which meant that, in a period of divided government, absolutely nothing would ever get done.

Austerity

In Europe, the word had a weaponized meaning: that, almost exactly as Naomi Klein predicted in The Shock Doctrine, faced with a crisis, any crisis, the world's bankers and governments would together put the needs of capital first, making giant cuts to spending even in the midst of five-year-long recessions and 25 percent unemployment rates. In the United States, there weren't real cuts — though the stimulus wasn't as large as some might have liked — and so the word conjured less a policy prerogative than a national mood. There just didn't seem to be any money around, in Washington especially, and little hope, after the tea party swept into Congress in 2010, of accomplishing anything of any scale.

Bailout

What you called government aid someone else got — the banks, the auto business, Fannie Mae and Freddie Mac.

The One Jailed Wall Street Banker

Yep, there was just one — an Egyptian-born trader named Kareem Serageldin.

Zombie Apocalypse

It's the only kind you can market in a zombie economy.

The Dark Knight Rises

Supervillain (and bank robber) Bane gives an Occupy-like speech outside a prison.

MMT

If the global financial crisis was our Great Depression, didn't we need our own Keynesianism? Modern monetary theory, a formulation of demand-side economics that suggests governments can print as much money as is necessary for expenditures and need to tax citizens only in order to keep inflation down, seemed closest, with its appealing contrarianism (and promise of expansive government stimuli).

The 47 Percent

Would anyone have believed, before the crash, that just about half the country was on the dole? Romney's gaffe certainly had more of an audience in the age of the Obama phone.

Populism

In Europe, centrist governments turned to austerity, which left victims of the crisis in even worse shape — in some cases — and created an opening for Trump-style extreme-right nativists. In the Netherlands, Geert Wilders, of the Party for Freedom, tweets about countries like his becoming "retarded Islamic Sharia-nations." In France, Marine Le Pen — daughter of the infamous Holocaust denier — has made the near-fascist National Front a major contender. Alternative for Germany, which aims to ban mosques, is now that country's largest opposition group.

Alt-right