While Monday's historic spike in the VIX may be fading from memory - for now - it is certainly the case that the short-vol imbalances have hardly been removed from the market: while the short VIX ETN industry may have been eliminated, following several "termination events" for ETNs such as the XIV, it represented only $3 or so billion in assets; as such it is a small fraction of the total systematic vol sellers, including Risk Parity funds, CTAs, vol targeters, annuity funds and according to Fasanara Capital, everyone else, in what is one massive, $22 trillion, low-vol bet.

Even more modest calculations suggest that as much as $1.5 trillion is invested in funds with volatility-linked strategies, still a colossal sum. From the WSJ:

In a prescient research paper published in November, Vineer Bhansali, founder of investment advisory firm LongTail Alpha, and Professor Larry Harris of the USC Marshall School of Business explained how such a dramatic move might happen, and warned that "the extraordinary growth of short volatility strategies creates risks that may trigger the next serious market crash."

The paper suggests that the growth in the use of such strategies and the correlation between them risked a dramatic reversal as investors scramble to cover their short positions.

To cover a short position, investors who are directly shorting volatility buy back the asset they sold in the first place—in this case, volatility.

Risk parity or volatility target funds are a similar source of potential further sharp moves. Such funds aim to invest in assets based on their volatility, rather than allocating funds in a predetermined way to different asset classes.

When volatility spikes, that strategy involves selling the newly volatile underlying assets and rotating to more stable holdings such as cash.

Messrs. Bhansali and Harris estimated that $1.5 trillion was invested in funds with volatility-linked strategies, a colossal sum capable of shifting global markets.

For now, however, the panic over the VIX surge has stabilized, and today the fear index is already down over 20%, tumbling from 30 to 22. Still, before everyone assumes that all is well and the crisis has been averted - when in reality what happened on Monday merely let out some of the record pressure within the vol complex - here is Bank of America's derivatives expert, Benjamin Bowler, explaining why what happened on Monday was a Minsky Moment for the VIX, and also why the real crash can only take place once the volatility panic in equities spreads to other asset classes.

* * *

Wake up call for short equity vol, by Bank of America's Benjamin Bowler and team.

US equity centric shock + short vol makes VIX ground zero

The sell-off in US equities Monday (S&P cash down 4.1%, futures down 5.4%) was the worst one-day S&P decline since 2011, and ended the 90 year record just set in recent weeks for the longest period without a 5% S&P pullback.

So far, the bulk of the stress has been equity centric (Chart 7), and by far the largest shock has been to US equity vol, where the moves in VIX and VIX futures exceeded anything in recorded history. Chart 8 compares VIX to the similar measures for US Treasuries (MOVE), FX (CVIX), and Gold (GVZ).

A "Minsky Moment" for the VIX

While we did not see short volatility positioning as large enough or levered enough to catalyze the next global crisis, we were concerned about the risk of an outsized VIX spike in 2018 with little forewarning, potentially amplified by a short vol positioning squeeze.

February 5th delivered exactly such a VIX spike, with the constant maturity VIX 1-month future recording its largest spike in history (by a wide margin) relative to the decline in US equities (Chart 11). Indeed, the 94.4% rise in the constant maturity VIX 1M future was nearly 17.5x as large as the -5.4% drop in e-mini futures, easily the largest stress beta recorded (data since Sep-07) and a large enough percentage rise to leave some popular short volatility strategies at risk of losing 100% of their capital.

Particularly striking was the acceleration in the vol spike between 4pm and 4:15pm (Chart 12), when the front-month VIX futures contract rose nearly 10 vol points and the second-month contract rose nearly 8 vol points. For context, the largest close-to-close move ever recorded in the constant maturity VIX 1M future was ~5.5 vol points in Brexit. A likely driver of the parabolic vol spike into the close on 5-Feb was the sizeable rebalancing needs of levered and inverse VIX products, which by our estimates may have bought ~$250mn vega or a record 26% of the day's volume ($930mn vega) traded in the front two VIX futures contracts.

Despite the pain likely being felt by some in the short vol community, it is important to remember that the size of potential losses here is a fraction of the broader active risk-taking market. For example, even if some popular short volatility strategies lose 100% of their capital, this would likely be several orders of magnitude less than the ~$1tn loss in S&P 500 market capitalization experienced on 5-Feb.

Note that with VIX futures now at a significantly higher base level and the short vol positioning embedded in "inverse VIX" products significantly de-fanged, an imminent repeat of the events of 5-Feb becomes less acute, in our view.

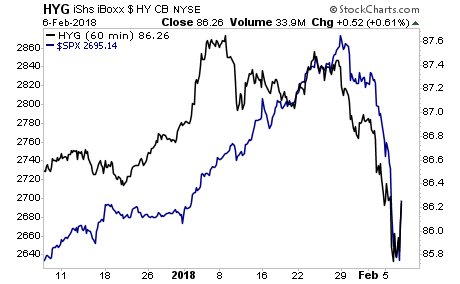

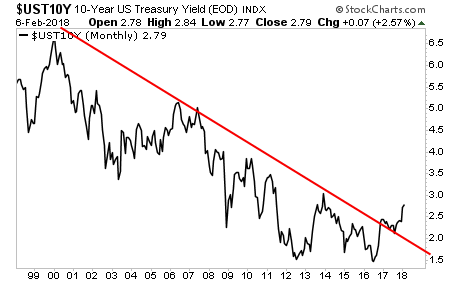

This is an equity tantrum not a bond tantrum which is comforting

While many suggest this shock was driven by concerns of inflation leading to faster than expected policy normalization (the right thing to be concerned about in our view), rates have been incredibly stable compared to past bond-led shocks such as the taper tantrum (Chart 9, 10). In fact, Treasuries rallied Monday in a flight-to-quality (perhaps aided by CTA positioning), but the fact this shock so far is very equity centric is positive. Key to understanding whether this is a short-term technical equity sell-off, which quickly reverses, or the beginning of something bigger, lies in where rates vol goes from here.