The Problem With Passive

Passive strategies, which are widely popular with individual investors, are often based on Nobel Prize winning portfolio theories about efficient markets and embraced by the banks and brokers that profit from selling the strategies. They are often marketed as "all-weather" strategies to help you meet your financial goals.

To be blunt – there is no such thing as an all-weather passive strategy, no matter the IQ of the person who created it. As we have repeated throughout this series, buy and hold/passive strategies are only as good as your luck. If valuations are cheap when you start passively investing, then you have a decent shot at meeting your financial goals. If, on the other hand, valuations are extreme and rich, you are likely to endure a multi-year period of low to even negative returns which would leave you halfway to retirement without much progress towards that goal.

That is not a hypothetical statement. It is simply a function of math.

Howard Marks, via Oaktree Capital Management, and arguably one of the most insightful thinkers on Wall Street penned a piece discussing the risk to investors.

"Today's financial market conditions are easily summed up: There's a global glut of liquidity, minimal interest in traditional investments, little apparent concern about risk, and skimpy prospective returns everywhere. Thus, as the price for accessing returns that are potentially adequate (but lower than those promised in the past), investors are readily accepting significant risk in the form of heightened leverage, untested derivatives and weak deal structures. The current cycle isn't unusual in its form, only its extent. There's little mystery about the ultimate outcome, in my opinion, but at this point in the cycle it's the optimists who look best."

Unfortunately, that was also a repeat of a passage he wrote in February 2007. In other words, while things may seemingly be different this time around, they are most assuredly the same.

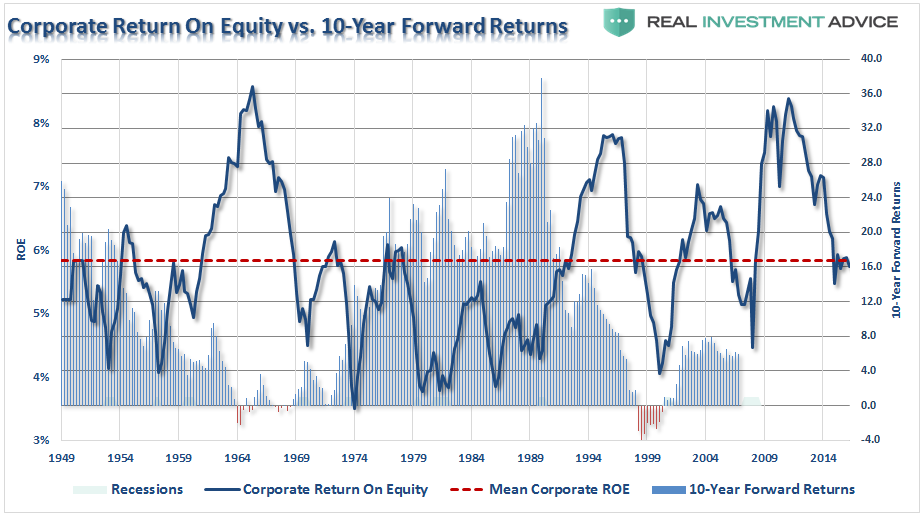

This brings us to the "Rule of 20." The rule is simply inflation plus valuation should be "no more than 20." Interestingly, while the rule is pushing the 3rd highest level in history, only behind 1929 and 2000, such levels suggest the market is more than "fully priced." Regardless of what definition you choose to use, the math suggests forward 10-year returns will be substantially lower than the last.

![]()

In a market where momentum is driving an ever smaller group of participants, fundamentals become displaced by emotional biases. As David Einhorn once stated:

"The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won't sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

There was no catalyst that we know of that burst the dot-com bubble in March 2000, and we don't have a particular catalyst in mind here. That said, the top will be the top, and it's hard to predict when it will happen."

Such is the nature of market cycles.

Missing The Target

The trouble with passive investing is best exemplified by the greatly flawed concept of Target Date Funds (TDF). TDF's are mutual funds that determine asset allocation and particular investments based solely on a target date. These funds are very popular offerings in 401k and other retirement plans as well as in 529 College Savings Plans.

When TDFs are newly formed with plenty of time until the target date, they allocate assets heavily towards the equity markets. As time progresses they gradually reallocate towards government bonds and other highly-rated fixed income products.

The following pie charts below show how Vanguard's TDF allocations shift based on the amount of time remaining until the target date.

![]()

The logic backing these funds and others like it are based on two assumptions:

You can afford to take more risk when your investment horizon is long and you should reduce risk when it is short.

Stocks always provide a higher expected return and more potential risk than bonds.

Let's address each assumption.

With regard to the premise of #1 about age and the propensity to take risks, we agree that an investor looking to withdraw money from their portfolio in the next year or two should be more conservative than one with a longer time horizon. The problem with that statement resides in our thoughts for #2 – there is no such thing as a steady state of expected risk and returns. The truth of the matter is that expected returns for stocks and bonds vary widely over time.

When an asset's valuation is low, ergo asset prices are cheap, the potential downside is cushioned while the upside is greater than average. Conversely, high valuations leave one with limited upside and more risk. This concept is akin to the popular real-estate advice about buying the cheapest house on the block and avoiding the most expensive. Investment risk is not a sophisticated calculation, it is simply the probability of losing money.

To demonstrate, the chart below plots average annualized five-year returns (expected returns), annualized maximum drawdowns (risk potential) and the odds of witnessing a 20% or greater drawdown for various intervals of valuations.

![]()

The graph shows, in no uncertain terms, that risks are lower and the potential returns are higher when CAPE is low and vice versa when valuations are high. Based on this historical evidence, we question how an investor can determine asset allocation based on a target date and the assumption that the expected risk and return do not fluctuate.

Currently, CAPE is at 32 which, based on historical data, implies flat to negative expected returns and almost guarantees there will be at least a 20% drawdown over the next five years. Granted, there is not a robust sample size because valuations have rarely been this high. However, given this poor risk/return tradeoff, why should a 2040 TDF invest heavily in stocks? Might bonds, commodities, other assets or even cash, have a higher expected return with less risk? Alternatively, during periods when stock valuations are well below normal and the risks are less onerous, why shouldn't even the most conservative of investors have an increased allocation to stocks?

To point out the flaws of TDF's the article is largely based on stock valuations and their expected risk and return. We do not want to convey the thought that investing is binary (i.e. one can only own stocks or bonds) as there are many ways to gains exposure to a variety of asset classes. Active management takes this into consideration before allocating assets. Active managers may largely avoid stocks and bonds at times, for the comfort of cash or another asset that offers rewarding returns with limited risk.

Simply, the goal of an active portfolio manager is to invest based on probabilities.

Math always wins.

You Aren't Passive

At some point, a reversion process will take hold. It is then investor "psychology" will collide with "leverage" and the problems associated with market liquidity. It will be the equivalent of striking a match, lighting a stick of dynamite and throwing it into a tanker full of gasoline.

When the "herding" into "passive indexing strategies" begins to reverse, it will not be a slow and methodical process but rather a stampede with little regard to price, valuation or fundamental measures.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will cause large spreads between the current bid and ask pricing for passive funds. As investors are forced to dump positions to meet margin calls, the lack of buyers will form a vacuum causing rapid price declines which leave investors helpless on the sidelines watching years of capital appreciation vanish in moments.

Don't believe me? It happened in 2008 as the "Lehman Moment" left investors helpless watching the crash.

![]()

Over a 3-week span, investors lost 29% of their capital and 44% over the entire 3-month period. This is what happens during a margin liquidation event. It is fast, furious, and without remorse.

Currently, with investor complacency and equity allocations near record levels, no one sees a severe market retracement as a possibility. But maybe that should be warning enough.

If you are paying an investment advisor to index your portfolio with a "buy and hold" strategy, then "yes" you should absolutely opt for buying a portfolio of low-cost ETF's and improve your performance by the delta of the fees. But you are paying for what you will get, both now, and in the future.

However, the real goal of investing is not to "beat an index" on the way up, but rather to protect capital on the "way down." Regardless of "hope" otherwise, every market has two cycles. It is during the second half of the cycle that capital destruction leads to poor investment decision making, emotionally based financial mistakes, and the destruction of financial goals.

No matter how committed you believe you are to a "buy and hold" investment strategy – there is a point during every decline where "passive indexers" become "panicked sellers."

The only question is how big of a loss will you take before you get there?