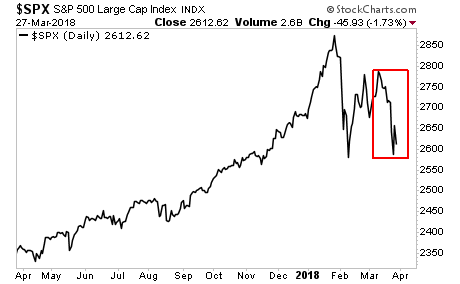

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).Trader: "The Probability Of 10Y Yields Collapsing Is Much Higher Than Most Realize"

One day after he correctly warned that equities have not yet bottomed - just hours before the Dow Jones tumbled from up over 200 to down over 400 points at one point as the tech sector imploded - this morning former Lehman trader and current Bloomberg macro commentator Mark Cudmore issues another warning, this time about Treasuries, which he thinks may be poised for a sharp spike higher as yields tumble. He explains why in his latest Macro View column below:

Treasuries Jump May Be the Start of Something Bigger: Macro View

The probability of Treasury 10-year yields collapsing is much higher than most investors seem to realize. The readjustment in pricing may be just getting started.

It's not going to take too much for serious discussion to begin over the possibility the Fed's hiking cycle may be at an end, or near an end, already.

This doesn't even need to become the base case for yields to slump, it just needs to become a plausible- enough outcome for the market to squeeze out the large speculative short position in Treasuries.

The building blocks for this narrative are already in place. Thursday's PCE inflation data may provide the required catalyst.

Financial conditions have tightened considerably in the last two months. Libor spreads have widened significantly -- because of structural issues -- but that still acts as effective policy tightening.

Trade, politics and commodities are all going to start weighing on the growth outlook. The slump in equities may soon be significant enough to be a concern for the Fed because of the impact on consumer sentiment, which has remained a bright spot in U.S. data, and the wealth effect.

As the manufacturing center for so much that the U.S. consumes, China's PPI has had an excellent correlation with U.S. CPI in recent years. The former is still trending down after both measures peaked in February 2017. The March data for both is due April 11. Given how industrial metals and agricultural prices have slumped this month, there are strong reasons to expect China PPI to slide again.

The technical break lower in yields was made Tuesday. Fundamentals are supportive of the move. Positioning is offside and therefore any related corrective adjustment will quickly add downside momentum to yields.

Tomorrow brings February's PCE data, supposedly one of the Fed's preferred inflation measures. The consensus forecast is for the core number to climb to 1.6% year-on-year. That paltry rate of inflation would still be the highest since since March last year.

A miss of just 0.1 of a percentage point and investors will start considering the possibility that inflation may already have peaked, and hence perhaps so has the Fed's rate-hiking cycle. That would put the cat amongst the short Treasury pigeons (positions).